The TCFD, also known as Taskforce on Climate-related Financial Disclosure, was created in 2015 by the FSB (Financial Stability Board) as a framework for the financial sector to consider climate change into their business. The framework is aimed at helping organizations to see the potential impact due to climate change on their primary business activities such as: revenue, cost, expenditures, assets, and liabilities. When first created, the TCFD was on a voluntary basis and aimed for only the financial sector, however as the urgency for climate action increases, the TCFD is gaining more and more support sector-wide and has already turned into a legally mandatory disclosure framework in the UK and New Zealand. So, what is the TCFD exactly and how can you align with the framework?

What is the TCFD?

The TCFD was created because of a problem that was not being addressed: without climate-related financial information, financial markets cannot price climate-related risks and opportunities correctly. And those risks and opportunities are becoming more evident than ever. The rapid changes in climate policies, new technologies and the growing physical risk of climate change have prompted reassessment of the values of virtually every financial asset. Hence, The TCFD was created as a framework based on a set of consistent disclosure recommendations for use by companies as a means of providing transparency about climate related risks, exposure, and opportunities. In doing so, one of the goals of the TCFD is to accompany more informed investment, credit, and insurance underwriting decisions with regard to climate change.

The TCFD compared to other existing frameworks

Several climate-related disclose standards exists and it is often difficult to examine which framework fits your organization best and how they differentiate from each other. The TCFD differentiates itself compared to other frameworks by focusing on financial implications. Many of the existing standards focus on disclosure of climate-related information, such as greenhouse gas (GHG) emissions and other sustainability metrics. However, a translation to the financial implications around the climate-related aspects of an organization’s business is often missing. Furthermore, due to its standardized disclosure guidelines, the TCFD is also a framework which stimulates comparable reporting between organizations within the same sector, industry, or portfolio.

Themes and recommendations

The TCFD is aimed for public companies and other organizations to consider climate change into their business and effectively disclose climate-related risks and opportunities through their existing reporting processes. To do so, they use four thematic areas of recommendations that represent core elements of how organizations operate. Those areas are: Governance; Strategy; Risk management; and Metrics & targets.

It’s important to note how these thematic areas are interlinked with one another. With governance being the overarching theme, each theme goes a level deeper and becomes more tangible. Hence, they all influence one another, as can be seen in the figure above. A short explanation of each theme can be read in the table below.

| Governance | Disclose the organization’s governance around climate related risks and opportunities. |

| Strategy | Disclose the actual and anticipated/expected impacts of climate-related risk and opportunities on the organization’s business’ strategy (for the short-, medium-, and long-term, including climate-related scenarios) and financial planning where such information is material. |

| Risk management | Disclose how the organization identifies, assesses, and manages climate-related risk. |

| Metrics & targets | Disclose the metrics and targets used to asses and manage relevant climate-related risks and opportunities where such information is material |

Recommendations are given for disclosure on each of these four thematic areas. The four overarching recommendations are supported by recommended disclosures that build out the framework with information that will help investors and others understand how organizations assess climate-related risks and opportunities. For example, the lowest level theme “Metrics & targets” consists of the recommendations to a) Disclose the metrics used by the organization to assess climate-related risks and opportunities in line with its strategy and risk management process; b) Disclose Scope 1, Scope 2 and, if appropriate, Scope 3 greenhouse gas (GHG) emissions and the related risks; and lastly c) Describe the targets used by the organization to manage climate-related risks and opportunities and performance against targets.

In addition to the four general overarching thematic areas, supplemental guidance was developed for the financial sector (banks, insurance companies, asset owners, asset managers) and certain non-financial sectors (energy, transportation, materials and building, agriculture food, and forest products) to highlight important sector-specific considerations and provide a more complete picture of potential climate-related financial impacts.

Read the full report of recommendations.

Want to know more?

Are you interested in the implications of the TCFD and would you like to know more about this and other frameworks? Watch our webinar about the TCFD and other leading frameworks, standards, and regulations.

View "Webinar CSRD and EU Taxonomy"

Enter your details to view our webinar, on the topic of corporate reporting, standards, and frameworks. We will be taking a deep dive into the CSRD and EU Taxonomy so you know what to expect from these upcoming regulations!

"*" indicates required fields

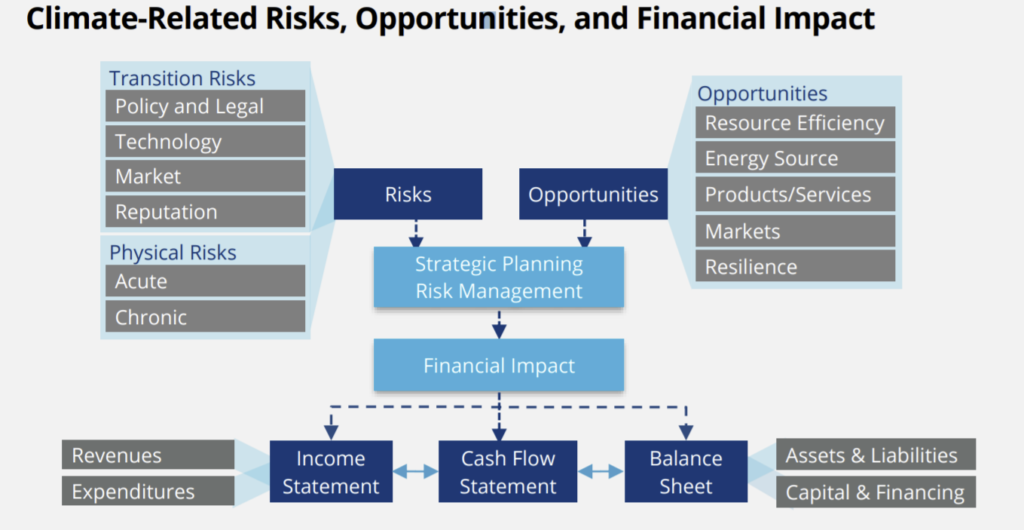

Risks and opportunities

The four thematic areas are based on risks and opportunities which occur due to climate change. The TCFD also provides a guiding framework in recognizing these risks and opportunities. Particularly, two different types of risks are identified. Transition risks and physicals risks. Transition risks include those risks related to the transition to a lower-carbon economy. Risks include extensive policy, legal, technology, and market changes to address mitigation and adaptation requirements related to climate change. Depending on the nature, speed, and focus of these changes, transition risks may pose varying levels of financial and reputational risk to your organizations.

Physical risk as a result of climate change can be event driven (acute) or longer-term shifts (chronic) in climate patterns. Physical risks may have financial implications for organizations, such as direct damage to assets and indirect impacts from supply chain disruption. Organizations’ financial performance may also be affected by changes in water availability, sourcing, and quality; food security; and extreme temperature changes affecting organizations’ premises, operations, supply chain, transport needs, and employee safety.

Opportunities also arise as efforts to mitigate and adapt to climate change increase. Opportunities can be found in resource efficiency and cost savings, the adoption of low-emission energy sources, the development of new products and services, access to new markets, and building resilience along the supply chain. Climate-related opportunities on each topic will vary depending on the region, market, and industry in which your organization operates.

The figure below illustrates how risk and opportunity due to climate change can affect the financial impact of your organization.

.

The seven principles

Besides the recommendations, risks, and opportunities, the TCFD also has seven principles on which it is build. These principles help to safeguard high-quality disclosures with the objective to enable users to understand the impact of climate change on their organization. The principles read as followed:

- Disclosure should represent relevant information;

- Disclosure should be specific and complete;

- Disclosure should be clear, balanced, and understandable;

- Disclosure should be clear over time;

- Disclosure should be comparable among companies within a sector, industry, or portfolio;

- Disclosure should be reliable, verifiable, and objective;

- Disclosure should be presented on a timely basis.

TCFD implications

Companies who use the TCFD framework for disclosure have noted to experience a multitude of benefits. Namely, increased brand value, reduced shareholder pressure and activism, increased diversity of investors, higher company value, and lastly a positive financial impact.

Companies also remarked that the TCFD can be used as a strategic piece in incorporating climate risk into their business and allows them to better understand how to build a resilient business in the face of climate change. In doing so, capital can be rightly allocated to those activities which reinforce the resilience of the organization. One of the other benefits of the TCFD is that it is easily implemented within the existing financial reporting process. So, existing reporting capabilities are used whilst ongoing collaboration and improvement are managed.

How can the TCFD help you?

The task force has 31 international members already with growing support with over 2,600 supporters worldwide. Its impact is increasing likewise with a binding practice in the UK and New Zealand, where all public listed companies with a premium listing will be required to comply or explain their activities with the TCFD’s requirements by 2023. Full mandatory disclosure of the TCFD across the non-financial and financial sector will be effective in the UK by 2025.

Furthermore, the TCFD recommendations are a basis upon which international accounting standard setters are building global standards for climate risk disclosure. Hence, it benefits to disclose in accordance with the recommendations made by the TCFD, not only to comply with (upcoming) regulations and standards, but also by means to channel investment towards sustainable and resilient solutions, opportunities, and business models.

Start today

Want to know how the TCFD can help your organization in the disclosure of climate-related risk? Don’t hesitate and contact us so we can discuss the possibilities!