Since its initial publication in mid-2020, the EU Taxonomy has been generating a lot of interest from companies and individuals alike. You can read all about the basics of the EU Taxonomy in our previous post. As of this January 2022, approximately 12,000 public interest companies are required to indicate whether their economic activities are eligible for the EU Taxonomy. How many companies’ activities are eligible for the EU Taxonomy? What are the implications if your company is eligible as of now? What other developments have taken place?

The new year has begun, which has brought us many new developments regarding the EU Taxonomy. In short, the EU Taxonomy is a classification system. It establishes if an economic activity is sustainable or not. The objective of the Taxonomy is to scale up sustainable investment to meet the Green Deal objectives and EU’s climate and energy targets for 2030.

As of the start of this year, 2022, it has been confirmed that if the CSRD will be accepted in its current form, all companies in the scope of CSRD have to report the extent to which their activities comply align with the EU Taxonomy. In other words, an estimated amount of 50,000 companies will have to apply the EU Taxonomy for reporting year 2024. This consists of all companies with over 250 employees and/or a balance sheet total of 20 million EUR and/or net turnover of 40 million EUR, and all listed SMEs.

The first delegated acts

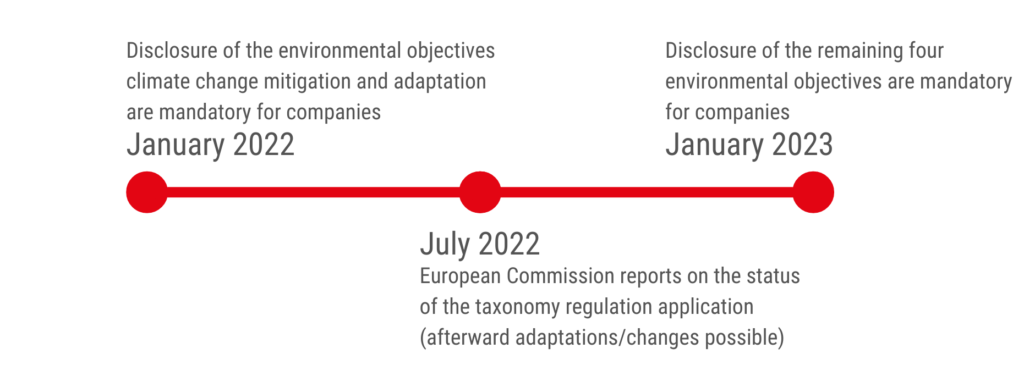

Moreover, the first delegated acts for the environmental objectives of climate change mitigation and adaptation have officially been adopted as of the start of 2022. This means that as of now, it is mandatory to assess and disclose the eligibility of your economic activities by the EU Taxonomy. The assessment should take place as the proportion of Taxonomy-eligible and Taxonomy non-eligible economic activities. Three KPIs are applied: total turnover, capital, and operating expenditure. Note that it is not yet mandatory to report the alignment of your activities per the EU Taxonomy. Only as of 2023 do companies need to report on the alignment of their economic activities.

But when is an economic activity aligned? As stated, an economic activity is aligned by the EU Taxonomy if it contributes substantially to at least one of the environmental objectives. Moreover, it cannot do any substantial harm to any of the other objectives. Lastly, the activity needs to comply with minimum safeguards. The first delegated act includes the environmental performance of almost 80 climate change mitigation activities and almost 100 climate change adaptation activities. This also includes do-no-significant-harm criteria across six environmental objectives. The criteria cover almost 80% of direct GHG emissions. The adoption of the first delegated act after multiple years of construction is an important milestone for the EU’s sustainable finance agenda.

The second delegated acts

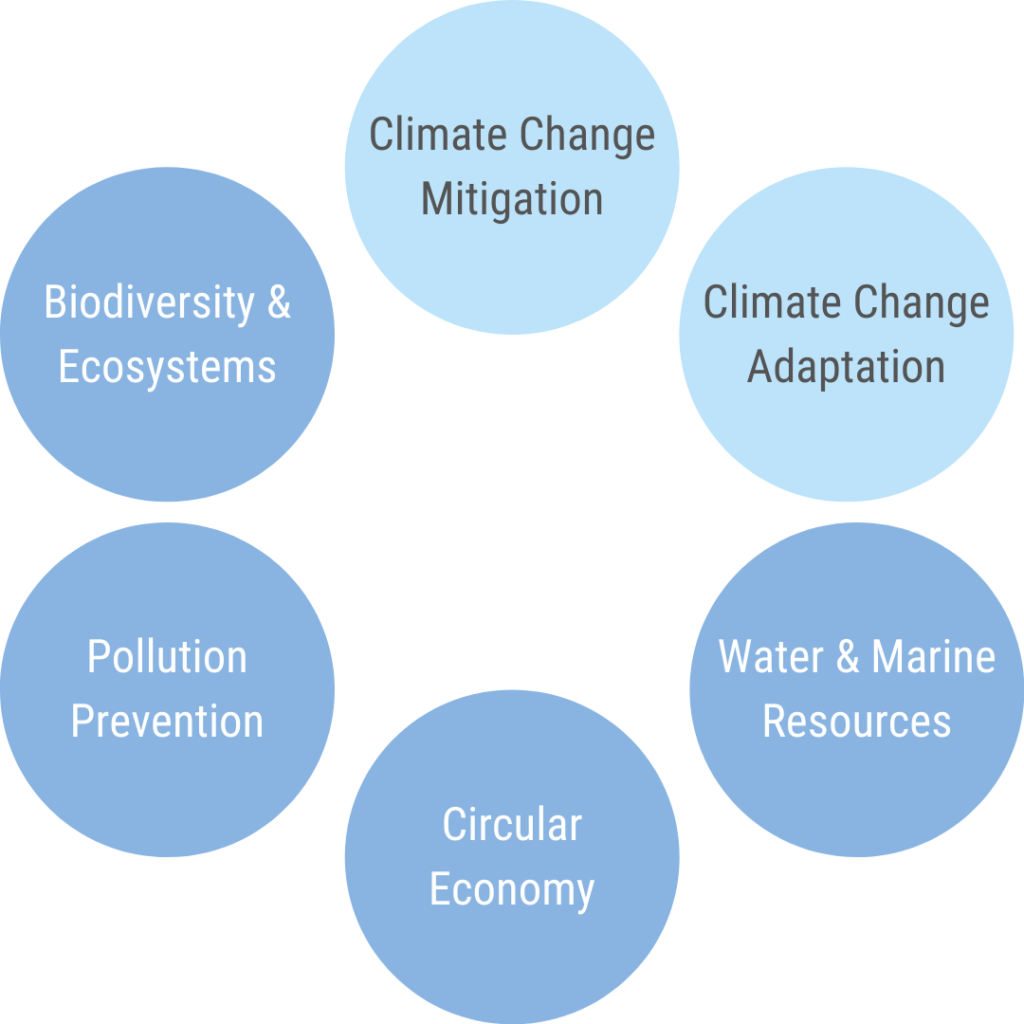

New developments in the EU Taxonomy have also occurred with the discussion of the second delegated acts of the remaining four environmental objectives. These environmental objectives are water & marine resources; circular economy; pollution prevention; and biodiversity & ecosystems. Although no final draft has been published due to delays, it is already clear that the number of sectors that have to report in accordance with the EU Taxonomy will be expanded. The other four environmental objectives will also expand the scope of the first two objectives. Namely, by including an additional six sectors that will need to report in accordance.

Delays are taking place due to discussions on the inclusion of a social Taxonomy and the extensive feedback they have received on the draft report. It is expected that the second delegated acts will be published around Q1 2022. We have created a small timeline with dates to keep in mind. Further developments which are expected to be taking place for the EU Taxonomy can be seen on the timeline.

What does the EU Taxonomy mean for your company?

Is your organization in one of the sectors which will need to report according to the EU Taxonomy? Would you like to know what this means for you? Fill out this survey and get a head start on discovering the requirements of the EU Taxonomy for the activities of your company.

Discussions taking place

Quite some uproar has taken place due to a new discussion. Namely, the plans to label nuclear energy and gas as ‘green’. A draft delegated act states that “it is necessary to recognize that the fossil gas and nuclear energy sectors can contribute to the decarbonization of the Union’s economy”. All European countries can weigh in on the newly drafted delegated act. Countries such as Germany, Austria, and Luxembourg fiercely oppose the proposition to label nuclear energy and gas as sustainable. According to them, nuclear waste could lead to devastating environmental disasters. Moreover, there are better low-carbon alternatives that should be focussed on. Including nuclear energy and gas could undermine the credibility and usefulness of the EU Taxonomy. This could lead to climate risk and regress the climate targets we are trying so hard to achieve.

However, France and Poland are in favor of nuclear energy in particular. They state it is a low carbon technology to ensure energy security in the transition towards renewable energies. Moreover, with the right protocols, they argue that nuclear energy does not do any harm to the other environmental objectives. Hence, nuclear energy can be labeled as sustainable. This discussion taking place is also one of the reasons the publication of the second delegated acts has been postponed.

What can Intire do for you?

The development of the EU Taxonomy has made it more evident than ever how essential data is. Only with valid data can companies map all their economic activities to the categories given by the EU Taxonomy regulation. If you fall under the scope of the CSRD, you will be legally obligated to report. However, even if you do not (yet) have a legal obligation, reporting per the EU Taxonomy can be beneficial for you too. Firstly, the EU Taxonomy can inform your corporate strategy in what sustainable activities to invest in, and where to divest from. Secondly, It can be used as a guideline to refine your company’s ESG strategy as it provides a clear structure on different sustainability topics, their interaction with each other, and important KPIs in an integrated manner. Lastly, even though you do not have a legal obligation yet, you will likely fall under the scope of the EU Taxonomy in the (near) future. Assessing your eligibility and aligning your activities ahead protects you for these future expansions.

Contact us now and let us discuss how to incorporate the EU Taxonomy into your company.

Hi Laura, thanks for the interesting contribution! One pressing question: What are the final (if applicable) timelines for Reporting EU Taxonomy and CSRD?

Important topic in communication with leads,

Kind Regards, Herman

Thank you for your comment, Herman!

The mandatory application date for the first two objectives of the EU Taxonomy (Climate change mitigation & Climate change adaptation) are already in action – as of this reporting year firms are mandatory to assess and disclose the eligibility of their economic activities if they fall under the EU Taxonomy. The latter four objectives (Water & marine resources; Circular economy; Pollution prevention; Biodiversity & ecosystems) are expected to have their mandatory application date as of the reporting year 2023 – depending on if the draft delegated acts get approved on time.

As of the CSRD, all large or listed companies within the EU will have to report according to the new CSRD as of the reporting year 2023. If the CSRD gets accepted in its current form, all those firms which fall under the CSRD also need to assess and disclose their economic activities by the EU Taxonomy.

I hope this answers your question. If you have any more, don’t hesitate to contact us!

Kind regards,

Laura (Intire)