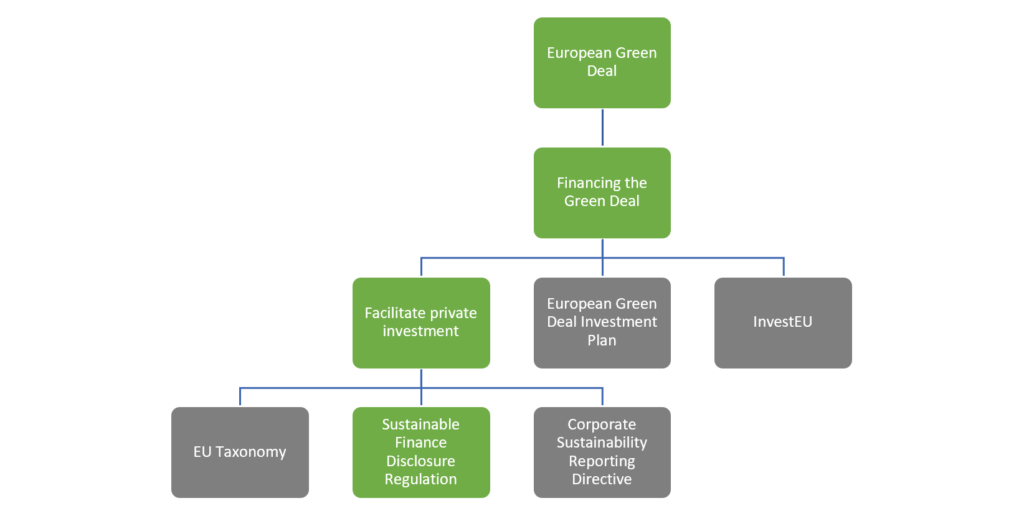

To achieve the climate goals that have been set by the European Green Deal, such as a 55% reduction of greenhouse gas emissions by 2030 compared to 1990, at least 1 trillion Euro in financing will need to be raised. A large share of this will come from the EU’s multiannual budget as well as other public funding. This is however not enough, which is why private investment needs to be stimulated as well. Following this line of thinking, three regulations have been introduced: the EU Taxonomy, the Corporate Sustainability Reporting Directive (CSRD) and the Sustainable Finance Disclosure Regulation (SFDR). The first two are applicable to all large companies, while the SFDR is purely for the financial market. This blog will delve into what the SFDR is, what it means for the financial market and why it is important.

If you wish to know more about the basics of the CSRD, read our in-depth blog post here!

What is the SFDR

The SFDR has been brought to life to regulate sustainability-related disclosures in the financial services sector. It contains mandatory ESG disclosure obligations for both financial market participants and financial advisers.

The main purpose of the SFDR is to increase transparency of sustainability impacts and risks in the financial sector, as well as to improve comparability between firms. Specifically, regarding the sustainability profile of funds. In practical terms this means that financial market participants, such as investment firms, need to address on multiple platforms what the sustainability risks and impacts are for all their financial products. Similarly, financial advisers will have to explain how they integrated the risks and impacts in their advice.

What are the effects of the SFDR

The most directly visible result of this regulation is the classification of funds in three categories. These are known by their respective articles in the SFDR: 6, 8 and 9.

- Article 6 describes the funds that do not integrate any type of sustainability considerations in the investment process and could include stocks that are distinctly unsustainable such as coal producers and tobacco companies.

- Article 8 refers to funds that are environmentally and socially promoting. This means that the financial product in some way promotes environmental or social sustainability. Additionally, funds are only classified under article 8 if the companies that are invested in follow good governance practices.

- And lastly article 9 covers the financial products that target sustainable investments. To be classified under article 9, requires the financial product to have sustainable investment as an objective and for an index to have been designated as a reference benchmark.

How is it linked to the EU Taxonomy

This classification system closely resembles the EU Taxonomy. The key difference is that while the EU Taxonomy is a classification system on an activity level, the SFDR is specifically for financial products. It should be noted that the EU Taxonomy builds on the SFDR. This means that in addition to the mandatory SFDR disclosures, firms will have to disclose extra information about the financial products they offer to comply with the EU Taxonomy.

Are you directly or indirectly impacted by the SFDR?

Are you trying to figure out what the best way to report is under the SFDR? Or perhaps an investor of yours has requested sustainability information from you to report? We can help you find out exactly what is needed and the best way to do it.

Simply contact one of our experts and we can discuss the best path forward!