The long-anticipated European Sustainability Reporting Standards (ESRS) have finally been established, marking a significant turning point for the Corporate Sustainability Reporting Directive (CSRD). As the CSRD’s mandatory disclosure timeline approaches, the clock is ticking, and the pressure on organizations is increasing. Many entities are entering uncharted territory, gearing up to report on diverse sustainability topics, leading to a steep learning curve. These new development process demands the development of new policies, procedures, and data collection systems, all under the pressure of the deadline. But there is a little relief: the CSRD’s phase-in measures.

What is a phase-in?

The European Commission acknowledges the substantial challenges that the new reporting regulations impose on organizations. In response, they have implemented phase-in measures to ease the transition. These measures grant organizations the flexibility to postpone reporting on particularly challenging or hard-to-obtain data. Instead, organizations can submit qualitative information or even pledge to report the data in the future, alleviating some of the immediate pressure.

What organizations can make use of the phase-in?

Every entity embarking on their CSRD journey, regardless of its scale or resources, benefits from the flexibility provided by the phase-in. The phase-in requirements are split into two different categories. The first category encompasses phase-in measures that are applicable to all organizations subject to the CSRD reporting requirements. The second category of phase-in measures is specifically designed for organizations with fewer than 750 employees. Recognizing the unique circumstances and resource constraints that smaller entities often deal with.

What reporting requirements can be phased in?

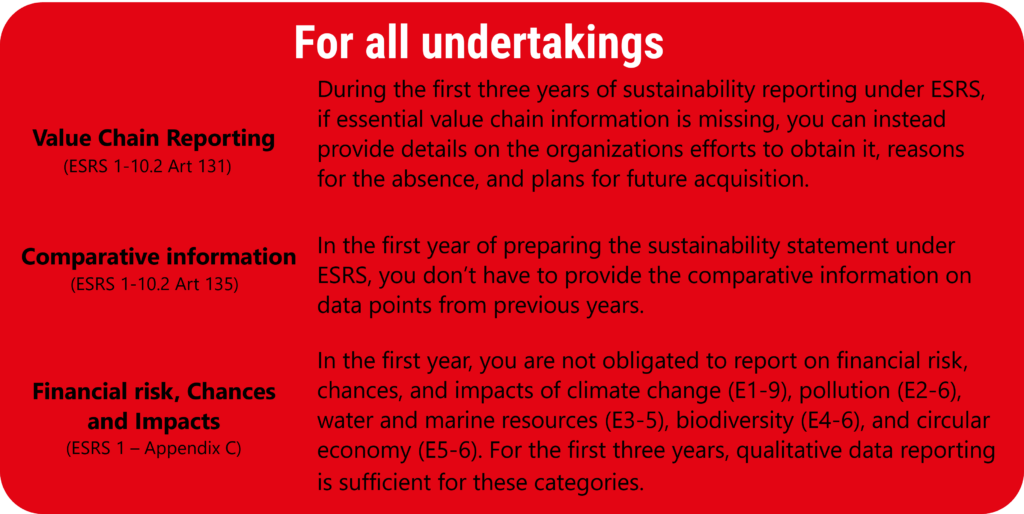

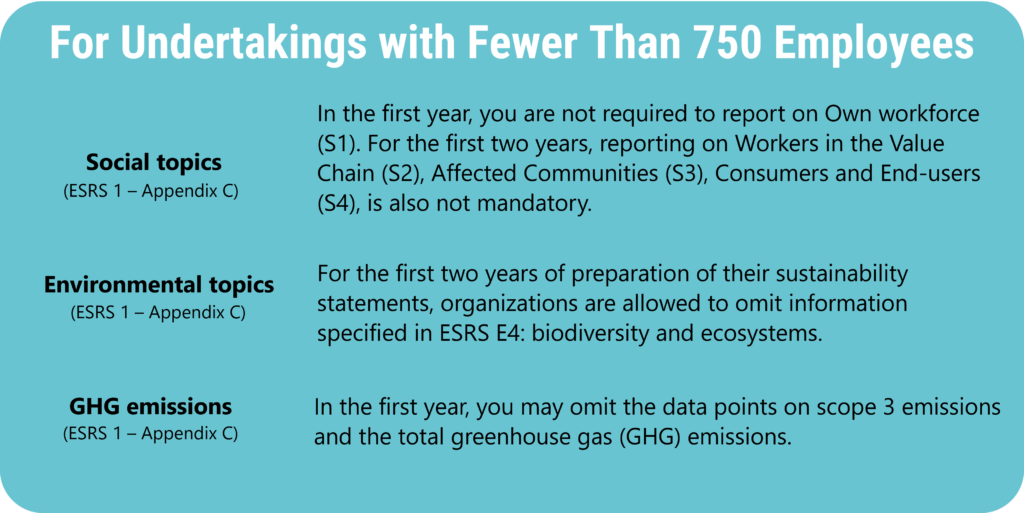

Only a select amount of reporting requirements can be phased in. To assist you, Intire has compiled an overview based on the final ESRS published in August 2023.

How to make progress on your CSRD reporting?

While the non-financial reporting process may still appear daunting, the relief provided by these phase-in measures is a welcome development. These measures enable organizations to adapt gradually to the new reporting requirements, ensuring that they can meet their obligations effectively and efficiently.

If you wish to delve deeper into the CSRD or explore how Intire can assist your organization in becoming CSRD-ready, please click here to learn more. Feel free to reach out to us to discuss how we can help your organization navigate this transformative journey.